Private passenger auto insurance rate changes approved or ordered for filings reviewed in 4th Quarter 2013

Author Archives: Admin2

Toronto Sun – Letters to the Editor, Jan. 21

Coverage, not abuse

Re “Ensuring insurance is a fair deal” (Christina Blizzard, Jan. 15): It isn’t just about what we are paying for auto insurance, it’s what we get when we have to access benefits like treatment, rehab, income replacement, and attendant care if we need it. Why should consumers have to take an insurer to court to get what they need when they’ve paid for coverage? Along the way victims are subjected to invasive, sometimes useless medical examinations by their insurer. There is virtually no oversight of this process — the CPSO won’t tell the public any details about complaints regarding these assessors and yet the public is legislated to attend these examinations. Accident victims endure a lot more than a few “slings and arrows” — our legislators need to pay attention to this industry. Drivers pay for coverage, not abuse. Motor vehicle accident victims “feel something akin to understanding” alright — we feel ripped off and understand that our government is letting it happen.

Rhona DesRoches

FAIR Association of Victims for Accident Insurance Reform

(There are two kinds of fraud in the auto insurance industry — fraud by con artists who try to bilk the insurers and fraud by insurers who refuse to honour valid claims)

http://www.torontosun.com/2014/01/20/letters-to-the-editor-jan-21-2

Is There a Place for Collaboration in Times of Disharmony? Seminars 2014

Wednesday, January 29, 2014

Wednesday, February 12, 2014

Wednesday, February 19, 2014

Wednesday, February 26, 2014

The auto injury benefits environment in which claimants, insurers, service providers and

legal professionals must function is in an unprecedented state of flux. The potential

for misunderstanding and frustration has never been higher. When positions become

hardened, is there still a place for collaboration to fulfill the spirit of the SABS? The

prominent members of the insurance, legal and health communities who will be speaking

at this seminar believe that there is. Full details:

Is There a Place for Collaboration in Times of Disharmony Seminar

Personal Injury Law: Service via Facebook should become the norm

To succeed in any such motion, counsel must establish that the person’s whereabouts for personal service are unknown despite diligent investigation; the Facebook profile belongs to the person in question; and the person is an active user of Facebook such that the claim will likely come to the person’s attention.

Personal injury judgement for trip and fall resulting in broken arm exceeds $200,000

An Ontario court recently awarded $107,765 to a women who broke her upper arm at the rotator cuff after stubbing her toe, tripping and falling on a city sidewalk in Caledonia, Ontario, southwest of Hamilton.

FAIR letter to the Dispute Resolution System Review, January 15, 2014

So when we talk about the cost of claims, we need to place some of the responsibility where it rightly belongs, with the most litigious of Ontario’s insurance companies whose cases form the better part of the volume at the Alternative Dispute Resolution Unit. Cases that are too often built on flawed medical opinion evidence provided by assessors who know they will not be held to task by their College oversight for their abuse of vulnerable accident victims

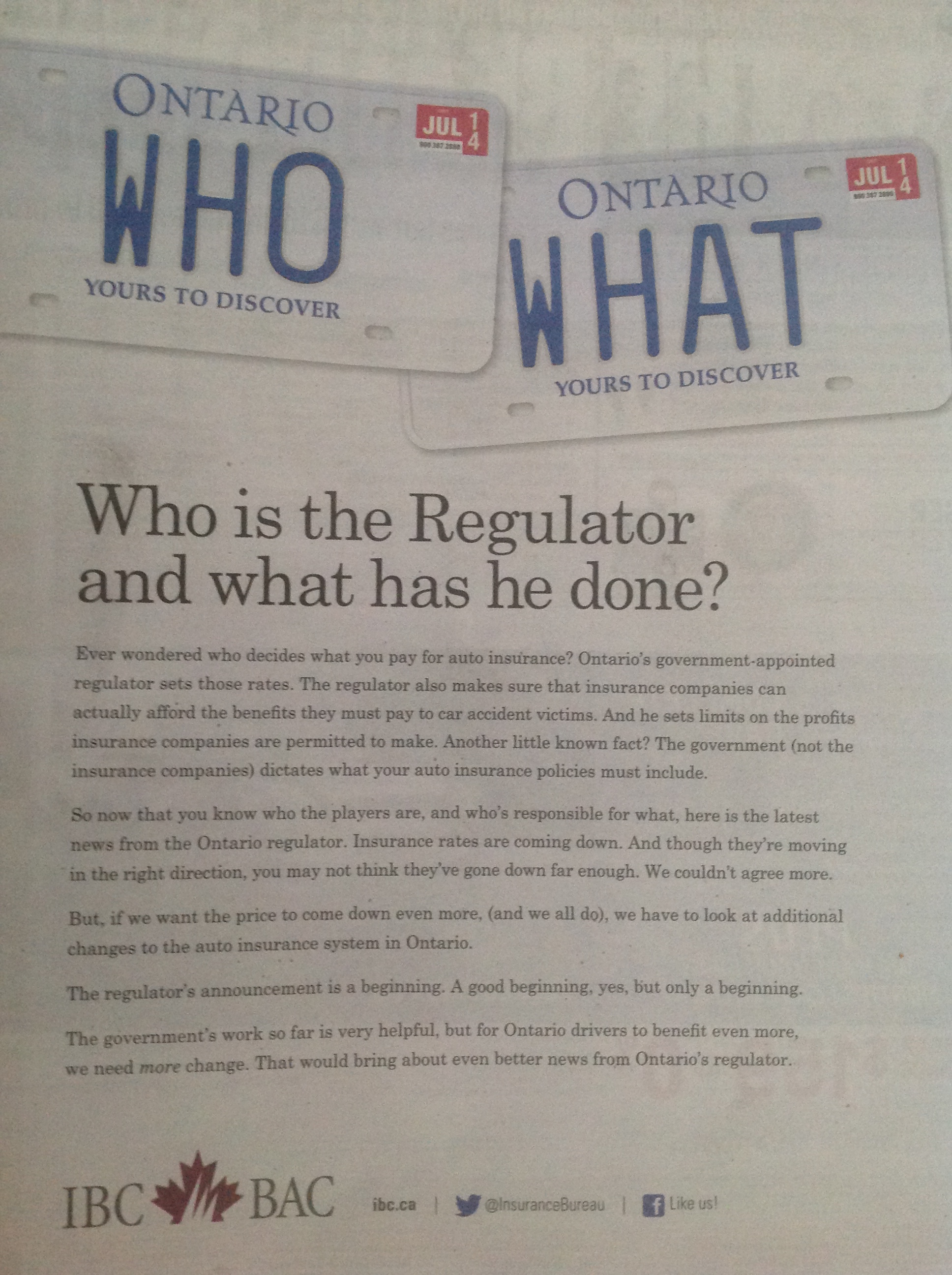

Who sets our rates and what the industry doesn’t want you to know

On January 16, 2104 the IBC placed advertising in many or Ontario’s major newspapers in respect to who sets the rates for Ontario’s drivers. In an ad entitled “Who is the Regulator and what has he done?” the Insurance Bureau of Canada asks and answers the question “Ever wondered who decides what you pay for auto insurance? Ontario’s government-appointed regulator sets those rates.” http://www.fairassociation.ca/?attachment_id=3005

{kind=link}

Here’s what Ontario’s regulators say:

FSCO’s Rate Approval Process : “Insurers must submit proposed changes to their rates to FSCO for approval along with supporting actuarial data. FSCO and its actuaries review this data and insurers’ assumptions regarding claims costs, expenses and investment income to ensure that, as required by law, the proposed rates are: just and reasonable, not excessive, and not going to impair a company’s long-term financial solvency. As a result of FSCO’s review, an insurance company may be required to amend its proposed rates before the rates are approved.” https://www.fsco.gov.on.ca/en/auto/rates/Pages/q4-2013.aspx

So why are we being told two versions? Why shouldn’t Ontario’s insurers take responsibility for the abysmal coverage we now have and the highest premium rates in North America? Who is driving up the costs here with expensive advertising – costs which are reflected in our premiums – money that could pay for the treatment that is denied to more than half of Ontario’s accident victims every year.

INJURIES DRIVE COSTS

Re “Time to speak up about car insurance” (Alan Shanoff, Jan. 12): We agree but there are a few points to note. The 2010 reforms were designed to address auto insurance abuse by those who derive income providing services to people involved in collisions. In 2009, the average cost of a medical/rehab claim in Ontario was $55,343, compared to $6,135 in Atlantic Canada and $2,776 in Alberta. It was clear the cost of a medical/rehab claim in Ontario was excessive, especially as a majority of claims were for minor sprains and strains. The 2010 reforms helped limit abuse. In 2012, the average cost of a medical/rehab claim was $26,594. Opponents of independent medical examinations (IME) have their opinion, but insurers rely on IMEs to provide fair and balanced second opinions. It’s regrettable that insurers have to resort to IMEs so frequently — a cost to the system that insurers would like to avoid. However, they’re used because of the large number of claims seeking to skirt reforms by claiming to have more serious injuries. IMEs are conducted by regulated health professionals who are members of regulated health colleges. Medical assessors are expected to attend to the interests of the injured person before all else. Colleges will impose sanctions if conduct is suspect.

RALPH PALUMBO

Vice-President, Ontario, Insurance Bureau of Canada

(The issue isn’t one of “opinion”. The reality is that genuine accident victims are constantly being assessed by biased individuals who have a vested interest in keeping costs to the insurance companies low. That’s entirely different from reducing fraud) Editor http://www.torontosun.com/2014/01/19/letters-to-the-editor-jan-19

2014 PRE-BUDGET CONSULTATIONS – speak up on auto insurance – write in

Have your voice heard – Those who do not wish to make an oral presentation but who wish to comment on the issue may send a written submission to the Clerk of the Committee at the address below by 5:00 p.m. on Thursday, January 23, 2014.

Liberals use auto insurance to promote own agenda

What other industry has to suffer the slings and arrows of political fortunes — and politicians telling them how much to charge for their product?

http://www.torontosun.com/2014/01/14/liberals-use-auto-insurance-to-promote-own-agenda